Research: portfolio rebalancing

This article is for informational purposes only and does not constitute financial advice. Past performance does not guarantee future results, and all investments carry risks, including the potential loss of principal.

Rebalancing a cryptocurrency portfolio is a strategy that helps maintain a consistent risk-return profile by periodically adjusting asset allocations. This involves selling overperforming assets and purchasing underperforming ones, thereby mitigating the risks of overexposure to any single asset. The primary benefit of rebalancing lies in the principle of mean reversion, where assets that have risen too much are sold off, and those that have fallen are bought, capitalizing on the potential for market correction. This approach helps keep the portfolio aligned with its long-term goals, even in a volatile market.

Key benefits of portfolio rebalancing:

- Risk Management: maintains the portfolio's target risk level by adjusting asset weights, preventing overexposure to highly volatile assets.

- Improved ROI: capitalizes on market fluctuations by selling overperforming assets and reinvesting in underperforming ones, following the "buy low, sell high" principle.

- Discipline and Objectivity: removes emotional decision-making, ensuring investments align with long-term goals and risk tolerance.

- Diversification: rebalancing ensures the portfolio remains well-diversified, reducing concentration risk and enhancing resilience to market shocks.

- Market Timing Efficiency: provides a systematic approach to capturing gains and reallocating funds without speculative timing.

What is Tezoro AI agent?

Tezoro AI agent is a smart contract that autonomously rebalances your portfolio through decentralized exchanges directly from your address, so you always have access to liquidity.

How do you use AI?

AI dynamically adjusts your portfolio parameters (asset weights and rebalancing thresholds) to maximize ROI. For example, if there is strong volatility in the market, then the AI makes the rebalancing thresholds wider. Or if AI indicates a trend in one of the assets, it can change its weight in your portfolio.

Which is better: Tezoro AI agent, hedge funds or ETFs?

Effective portfolio management involves diversification not only across asset classes but also across the tools and strategies used to manage those assets. Each approach — be it Tezoro AI Agent, hedge funds, or ETFs — offers distinct benefits that can complement one another. Combining these methods allows investors to balance risk, enhance returns, and adapt to changing market conditions in a thoughtful and comprehensive manner.

The table below provides a comparison of these tools, offering insights to help you integrate them into a well-rounded investment strategy.

| Parameter | Tezoro AI Agent | Hedge Funds | ETFs |

|---|---|---|---|

| Minimum Investment | No minimum | $100,000–$1 million | No formal minimum but costly entry for diversification |

| Dynamic Rebalancing | Yes (real-time, AI-driven) | Delayed (manual strategies) | No (static allocations) |

| Asset Coverage | All crypto assets | Concentrated on BTC, ETH, and a few others | Bitcoin and Ethereum only |

| Security | Non-custodial | Custodial | Custodial |

| ROI | We work hard to make it high | Moderate (varies by fund performance) | Moderate (taxes on distributions) |

| Risk Diversification | Maximum (broad asset coverage and smart allocation) | Limited (focus on few assets) | Limited (static allocation to a few assets) |

| Anonymity | High (no KYC required, full privacy) | Low (full KYC and personal data required) | Low (full KYC and regulatory oversight) |

| Fees | 2% management fee per year | 20% performance fee + 2% management fee | Expense ratio: 0.5%–1% annually |

Diving deeper into portfolio rebalancing

This research simulates performance of different portfolios based on historical data. We compare the ROI of these portfolios with a non-rebalanced portfolio of the same assets, BTC performance, and more. For clarity, we use the most effective rebalancing thresholds, but research shows that the range of effective thresholds is very wide. Each rebalancing transaction incurs a 0.3% commission.

Objectives

- Determine which strategy brings higher ROI: a rebalanced portfolio, a non-rebalanced portfolio, or a bet on a single asset.

- Calculate the ROI of portfolio rebalancing under different scenarios: if you made a lucky investment, an unlucky investment, a BTC-focused investment, or an "average" investment in blue chips.

- Identify which rebalancing thresholds show the highest ROI for each portfolio type.

- Discover which long-term BTC-focused strategy shows higher ROI: hold only BTC or create a portfolio of BTC and USD and rebalance it regularly.

Portfolio examples

Rebalancing by time

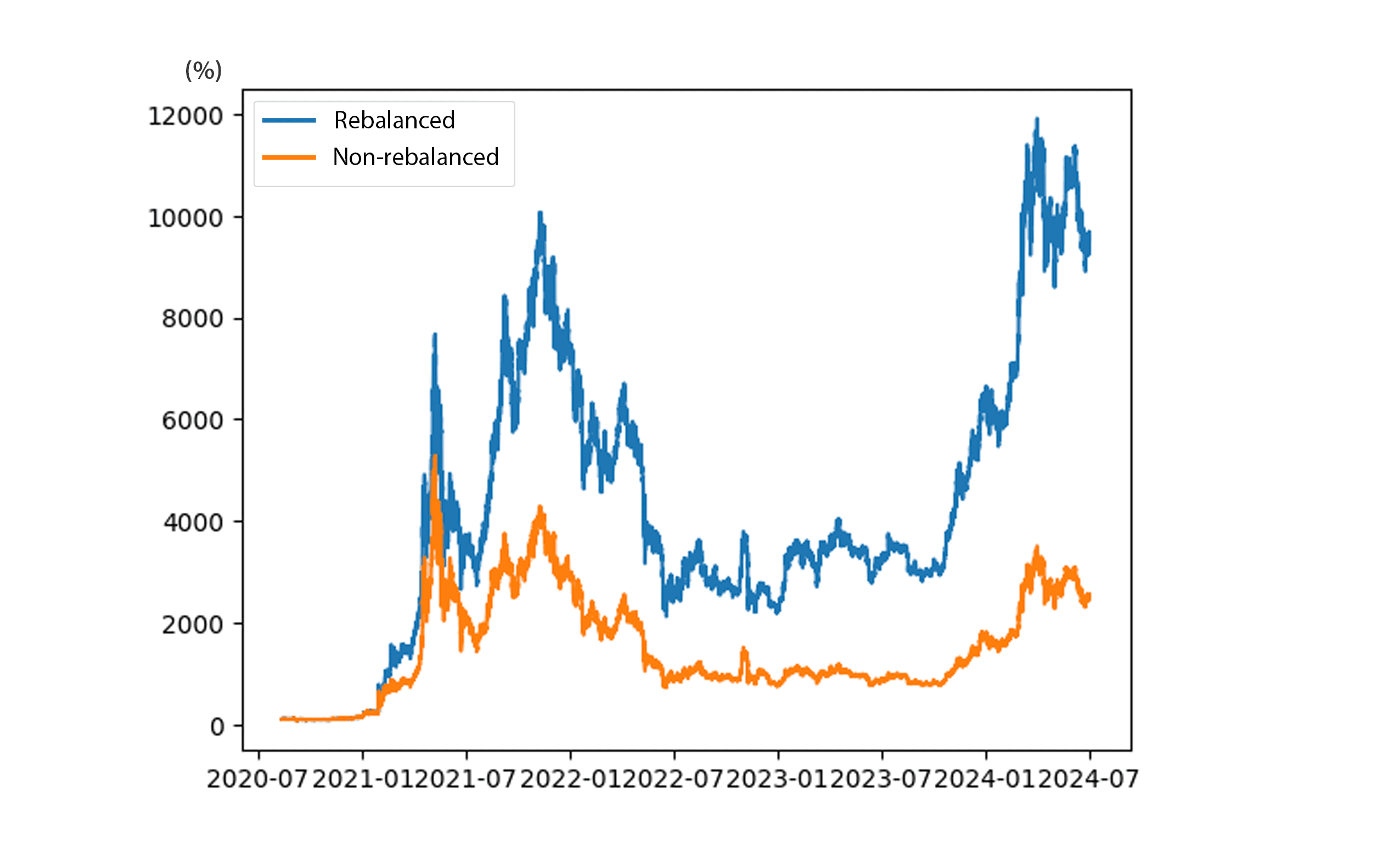

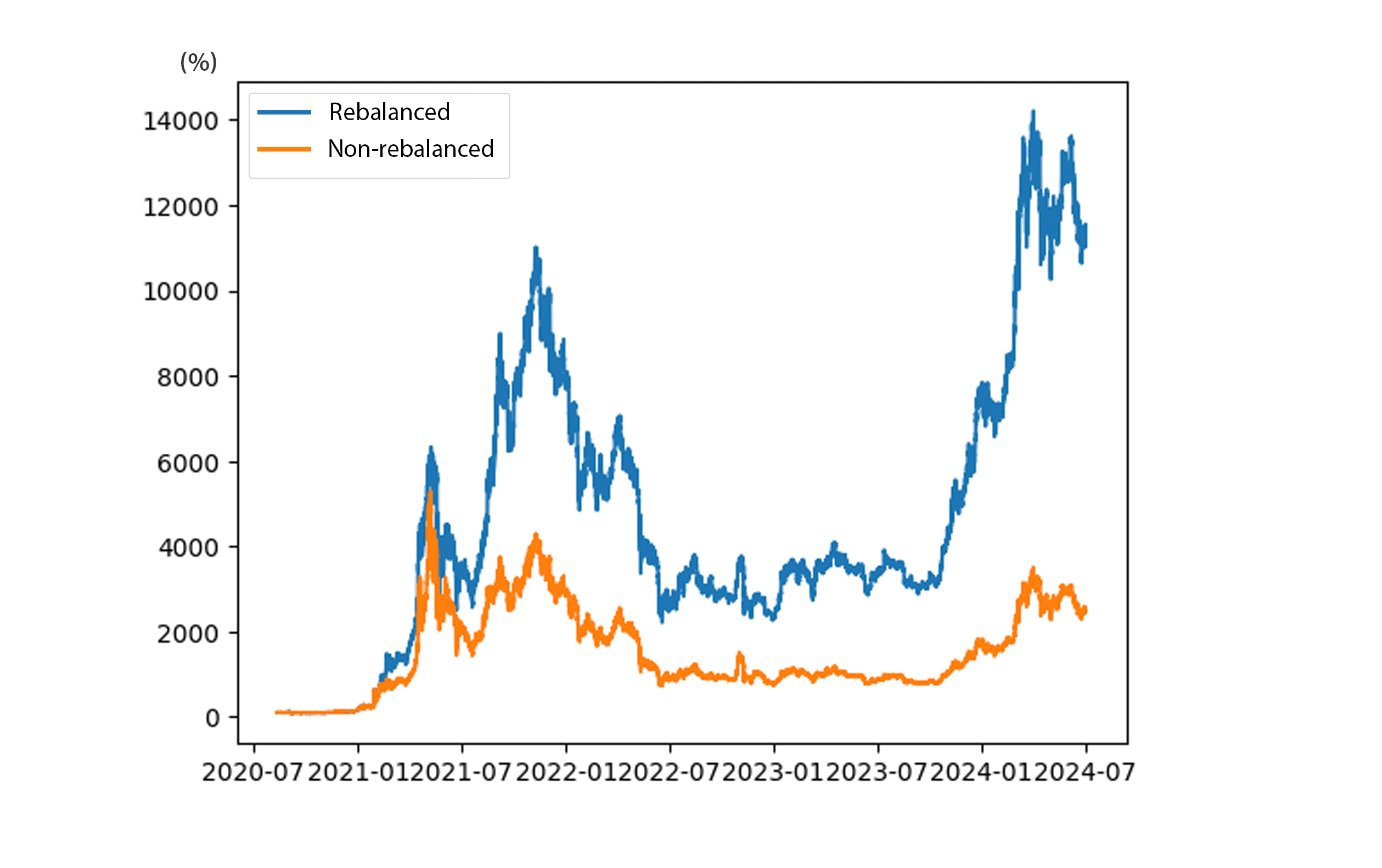

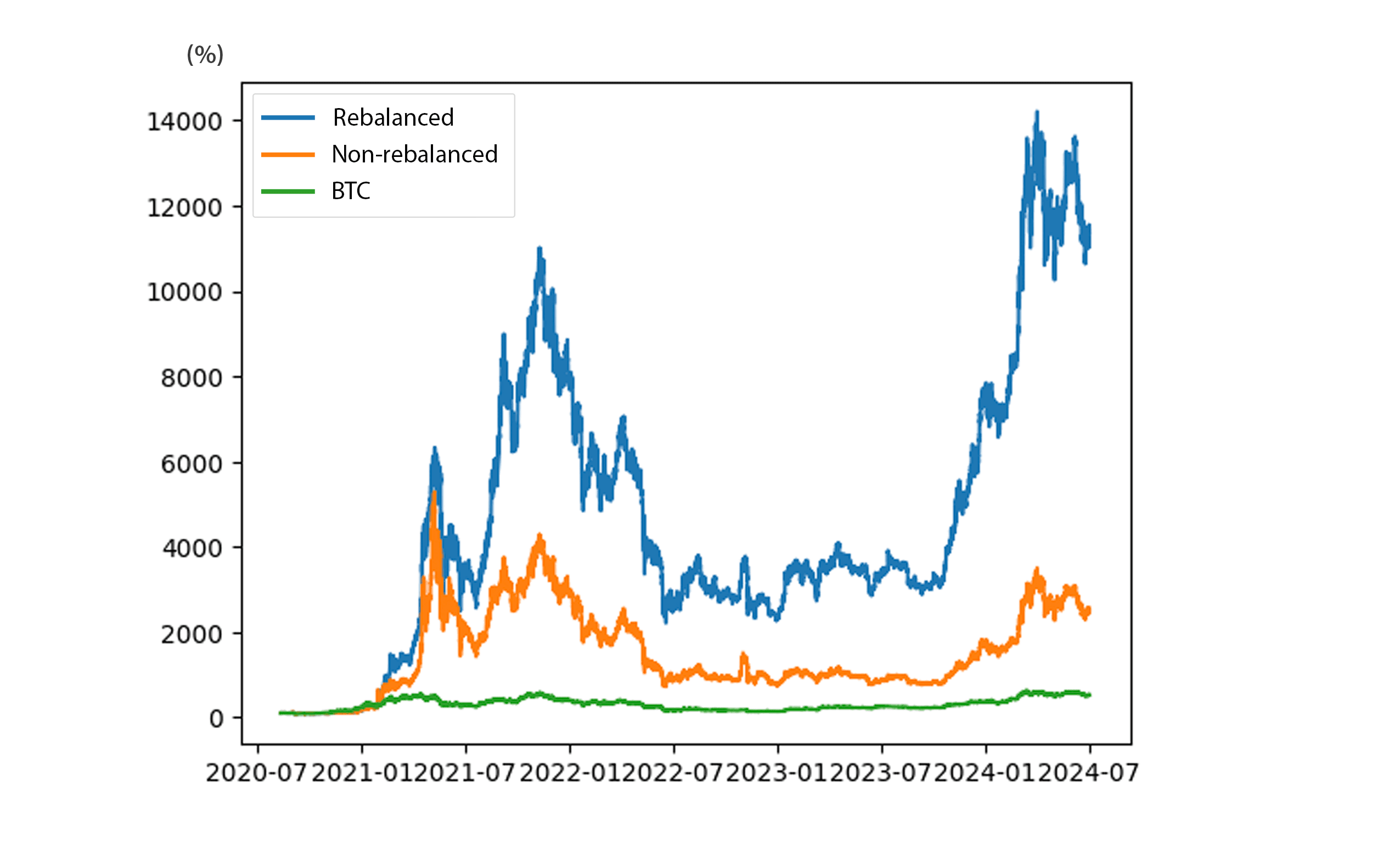

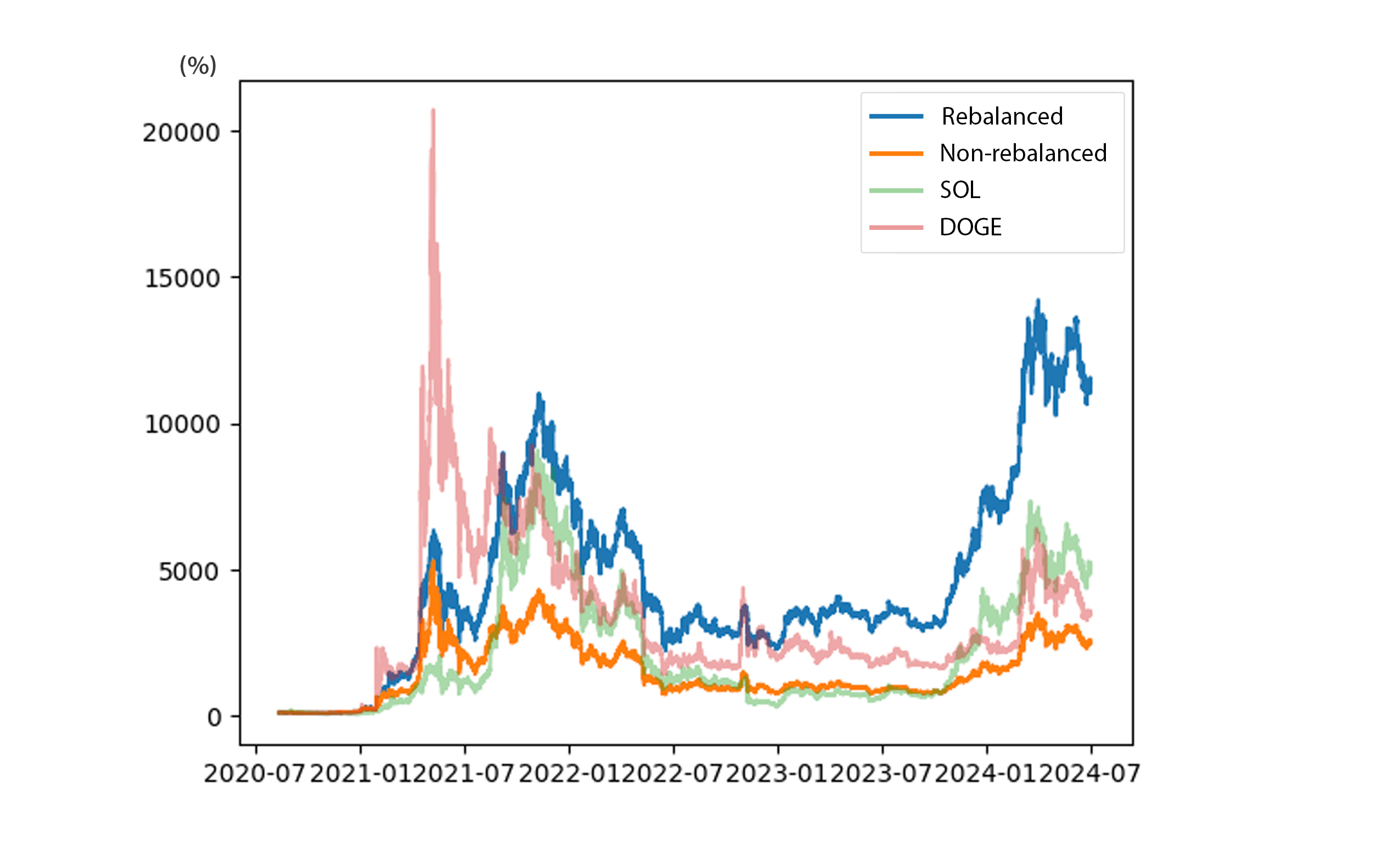

Portfolio of BTC, ETH, SOL, BNB and DOGE (20% each) rebalanced by time-based threshold over 4 years (from August 2020 to July 2024).

The most effective time-based threshold provided a return of 9433% in four years. It outperformed a non-rebalanced portfolio (2422% ROI) of the same assets by 7010%.

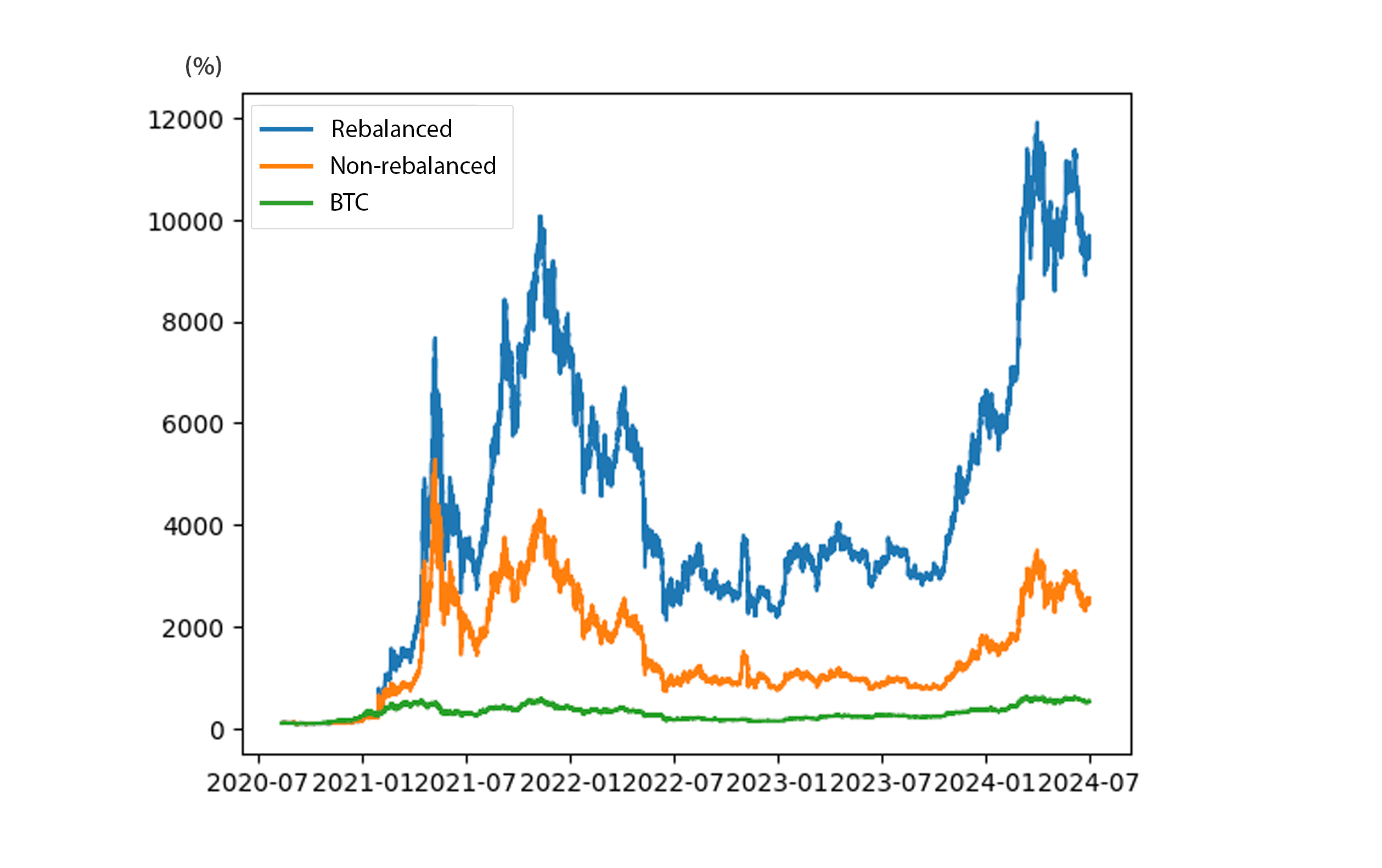

The rebalanced portfolio outperformed BTC (531% ROI) by 9001%.

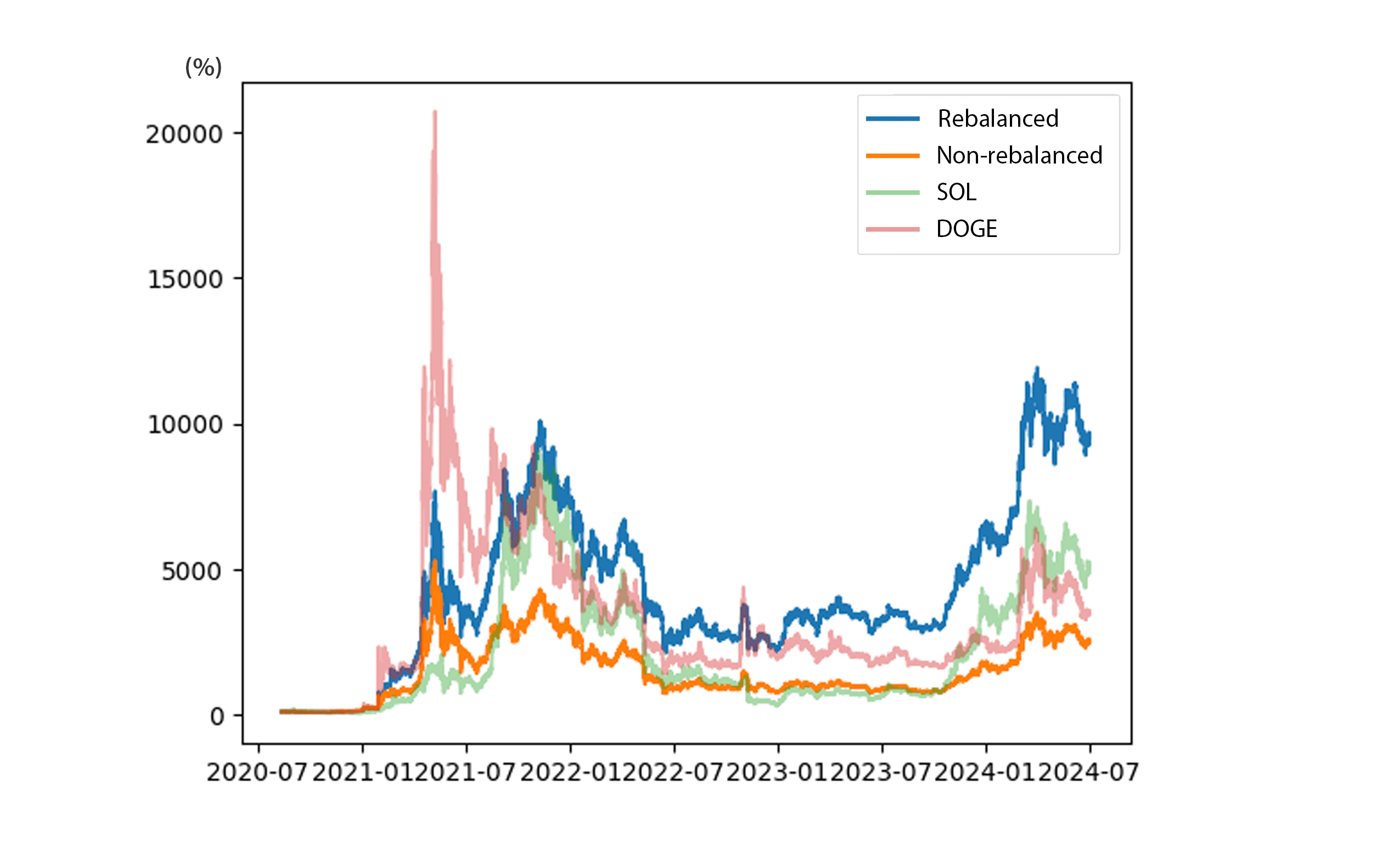

Moreover, the rebalanced portfolio outperformed each of the assets individually, even though its risk was diversified. Thus, the rebalanced portfolio outperformed ETH by 8661%, SOL by 4382%, BNB by 6953%, and DOGE by 6053%.

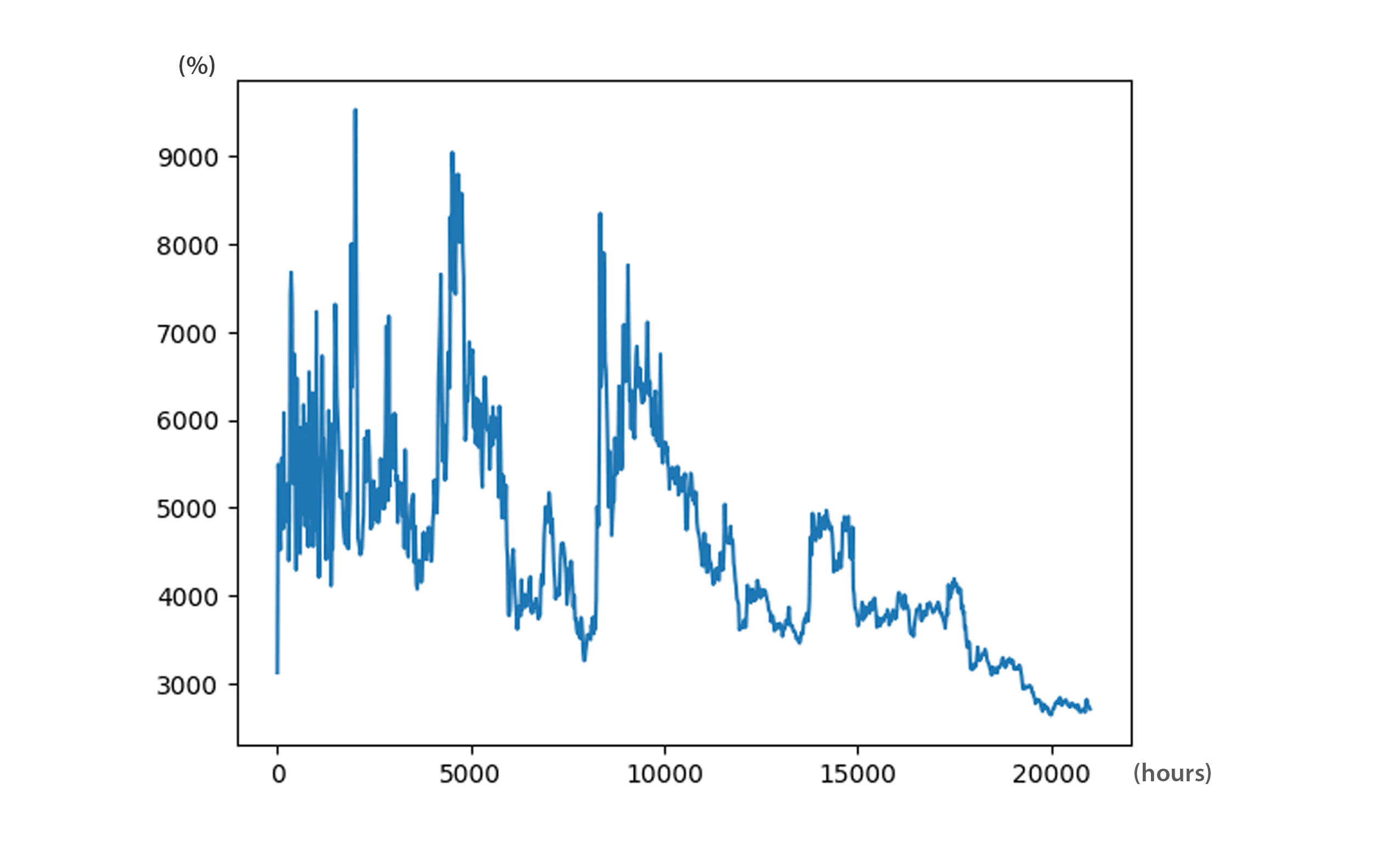

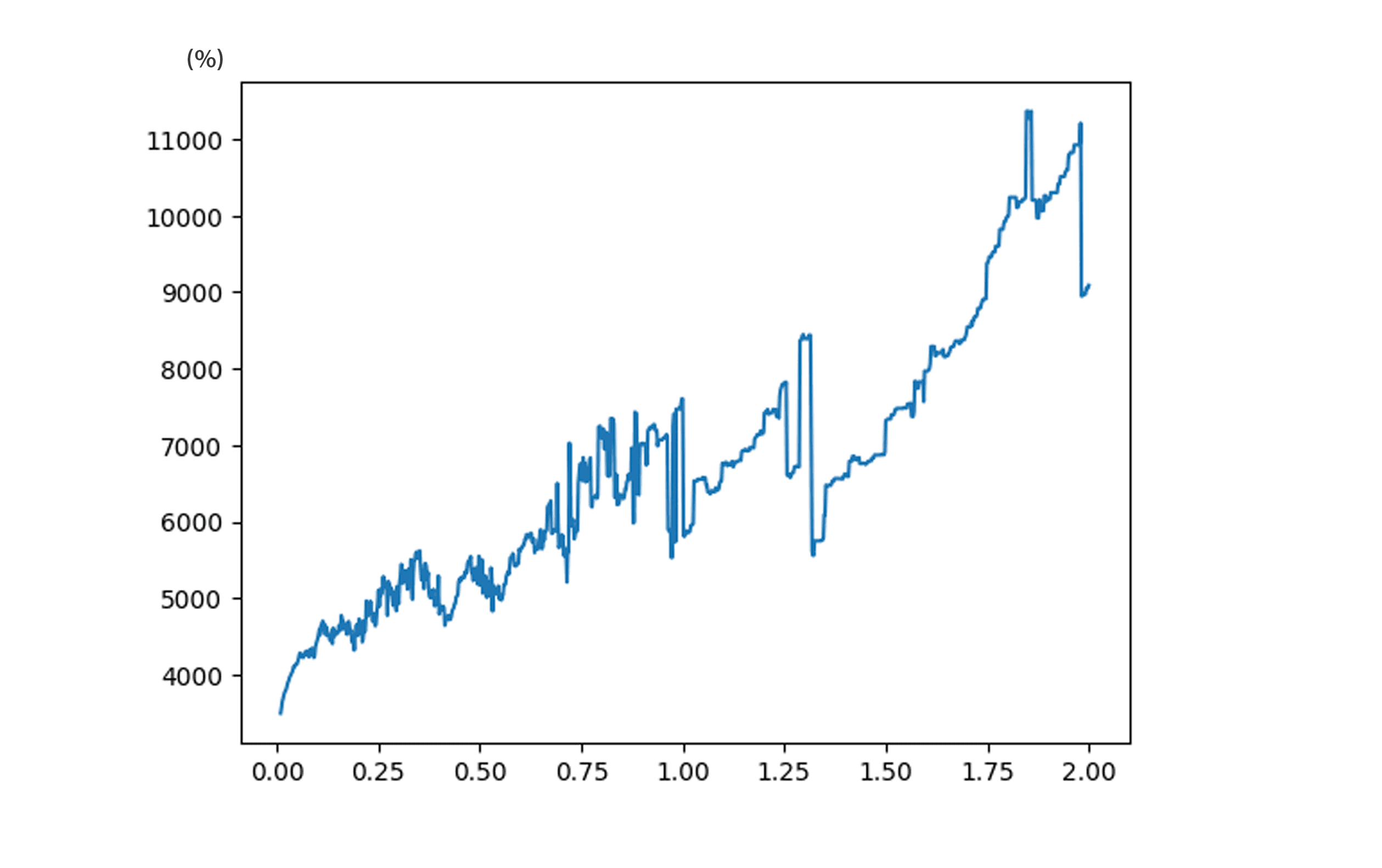

The best result was shown by the rebalancing threshold of 1442 hours (rebalancing every two months). However, as you can see in the chart below, any time-based threshold outperformed a non-rebalanced portfolio (2422% ROI). Moreover, there is a large zone of thresholds from 100 to 5000 hours, the results of which exceed the return of each of the assets separately.

Rebalancing by ratio

Portfolio of BTC, ETH, SOL, BNB and DOGE (20% each) rebalanced by ratio threshold over 4 years (from August 2020 to July 2024).

The most effective ratio-based threshold provided a return of 11262% in four years. It outperformed a non-rebalanced portfolio of the same assets (2422% ROI) by 8840% in the same period.

This rebalanced portfolio outperformed BTC (431% ROI) by 10832%.

Just like the time-based thresholds, the ratio-based rebalanced portfolio has outperformed each of the assets it consists of: ETH by 10491%, SOL by 6211%, BNB by 8782%, and DOGE by 7883%.

The best result was shown by the rebalancing threshold of 84%. As in the case of time-based thresholds, any rebalancing by ratio outperforms a non-rebalanced portfolio (2422% ROI).

Conclusion

- Each rebalanced portfolio with the most efficient rebalance threshold significantly outperformed a non-rebalanced portfolio of the same assets. In many cases, almost any rebalancing threshold would produce a higher ROI than a non-rebalanced portfolio - the zone of profitable thresholds is very wide.

- A rebalanced portfolio with one asset that has dramatically lost market value still shows a 3x higher ROI than a non-rebalanced portfolio of the same assets.

- The “lucky” portfolio portfolio that was rebalanced over four years using the most effective ratio-based threshold outperformed a non-rebalanced portfolio (2422% ROI) by 8840% and produced an ROI of 11262%.

- The BTC-focused portfolio (50% BTC and 50% USD) that was rebalanced over 6.5 years using the most effective time-based threshold outperformed a BTC-only portfolio by 104%, while having 50% lower risk.

- The “lucky” portfolio of multiple different assets not only significantly diversified risk compared to investing all assets in one token, but also outperformed each asset individually.